The Patrick administration is placing a lot of emphasis on raising the hotel room occupancy tax limit and creating a local option meals tax to raise municipal revenues and shift local fiscal reliance away from property taxes. Communities across the commonwealth are clamoring for revenues to support public services, most notably public K-12 education.

There is a lot of rhetoric bandied about in the political arena regarding taxing and spending and much of it is unclear. The word "revenue" seems to have replaced the word "tax" for all intents and purposes.

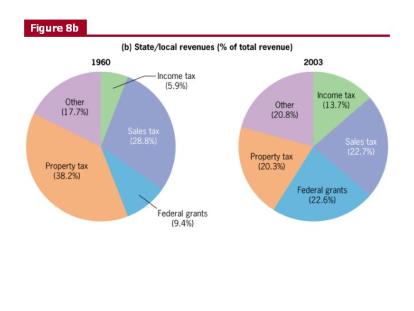

Consider Figure 8b. Nationwide from 1960-2003 property taxes as a percentage of total state and local revenues declined from 38.2% to 20.3%, but Massachusetts does not follow this trend. In fiscal year 2004 property taxes accounted for 52.9% of municipal revenue sources, up from 46.1% in 1988 (2004 dollars) according to the 2005 Municipal Finance Task Force report, "Local Communities at Risk." The report further suggests that Education spending receives the bulk of local spending and has grown from 46% to 50% of local government expenditures from fiscal year 1987 to 2004.

Source: Gruber (2005)

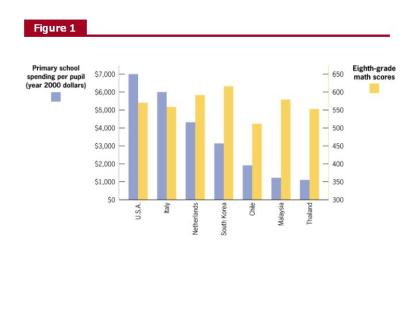

So while we’re spending more on education, is it paying off? In Figure 1. Gruber illustrates that nationally the United States ranks at or near the top globally for primary school spending per pupil, yet eighth-grade math scores in countries like the Netherlands, South Korea, Malaysia, and Thailand are competitive with or surpass the scores of our children, at a fraction of the cost. So, does throwing more money at the problem constitute the solution for Massachusetts?

Source: Gruber 2005

Though I’m not an economist, raising and creating new taxes ensures what is known as deadweight losses and inefficiencies in the marketplace. On the margins taxes generally price some people out of the market for goods and services indicating in this case that fewer meals will be sold and hotel rooms rented. In economic parlance this means that some trades between consumers and producers will be blocked that otherwise would be made. For establishments operating close to the margin of profit, taxes could be a factor that forces them to close or contract their business and lay-off staff, thereby reducing income taxes collected by the state and federal governments. I don’t know if these fiscal impacts have been studied, but if the new taxes collected are then given back to communities and used to benefit society’s welfare these new taxes are deemed justified.

Here are some excerpts from the website of the Massachusetts Municipal Association (MMA) regarding the proposed new taxes. Note the absence of a public referendum to adopt the meals tax, unlike Proposition 2 1/2 or debt exclusion overrides. It’s no wonder Higgins and other local leaders are stumping for this tax, they don’t have to follow the will of the people in order to adopt it:

"Local Option Taxes: The governor’s plan would authorize cities and towns to adopt a local sales tax on meals in addition to the current 5 percent state sales tax. Local acceptance of the tax and the rate, up to 2 percent, would be voted by the municipal legislative body, generally town meeting or the city council with the approval of the mayor. The MMA also has filed legislation to allow a local meals tax. For fiscal 2006, the state’s 5 percent sales tax on meals raised almost $600 million for state coffers.

The partnership plan would allow municipalities to increase from 4 percent to 5 percent the maximum local room occupancy excise in addition to the current 5.7 percent state excise. With almost all eligible cities and towns imposing the 4 percent maximum rate last year, the local room tax raised almost $82 million. The state also requires an additional 2.75 percent levy in six cities for convention center financing.

The Department of Revenue would collect both the state and local portions of the new municipal tax, as it does now. Twenty-five percent of the local portion of any of the new local taxes imposed after July 1, 2007, would be transferred to a special state fund to be used to reimburse cities and towns for property tax abatements under clauses 41, 41B and 41C of Section 5 of Chapter 59. (We had better look up those clauses for the specifics!-dgl) The balance would be distributed as general local revenue to cities and towns that accepted the tax in proportion to the dollar amount of sales of taxable meals and room occupancy in the municipality."

How might this impact Northampton? According to the Massachusetts Department of Revenue (MDOR) here is the breakdown in hotel/motel taxes collected in the city of Northampton in thousands of dollars for fiscal years 1999-2007.

- 1999-288.5

- 2000-310.9

- 2001-286.4

- 2002-365.8

- 2003-313.2

- 2004-336.3

- 2005-329.3

- 2006-359.4

- 2007-230.6*

*1/2 year

These figures average out to $323,700 not counting 2007. If the rate was to increase 25% this would increase the average by about $80,930 annually. It remains unclear how the proposed Hilton Garden Inn in the Round House parking lot would impact these figures.

Now lets examine another component of the municipal tax package. The MDOR has two years of meals tax data available. Here is the year-end data in thousands of dollars for taxable meals receipts. The state lists Northampton as having 120 eateries.

- 2004-54,665.7 **Far below is the state’s disclaimer on this data.

- 2005-56,600.7

The two year average is $55,633,200 and the following represents projected tax receipts based on that average and different percent levels.

- 3%- $1,668,996

- 2%- $1,112,664

- 1%- $556,332

Now this next part is a bit confusing-maybe Boston officials have access to some of the financial information the state does not have access to. The MMA website has a Municipal Partnership Act resources section. Contained therein is a spreadsheet of projected revenue increases for all 351 commonwealth communities. It’s called "Local Revenue Proposal Allocation; Numbers and methodology developed by the City of Boston, April 10, 2007." That’s all it provides so the source of these numbers is a bit of a mystery. For Northampton this sheet lists the following projected tax revenues in thousands of dollars:

- 142.4 telecom (from removing the property tax exemption on telephone poles, lines, etc.)

- 992.4-1% meals tax (We need to learn more on this because a 3% meals tax would provide the city $2,977,200 by this estimate, almost twice what I calculated above.)

So whose figures do we choose to believe? Maybe neither, but that is the reality behind setting public policy, perception can be more important than accuracy.

**The figures far above reflect compiled raw data from tax returns for the Sales Tax on Meals.

Please note that there are certain limitations to the data, when broken down into local groupings. Businesses that operate in more than one location in Massachusetts may be able to file a single sales tax return covering sales of meals at all of the location in the state. In the data kept by DOR, these sales would all be attributed to the address listed on the return.

For example a business has two restaurants: one in Northampton and one in Amherst. This business files a single return listing sales of meals from both locations. The address listed on the return is that of the Northampton location. In this case, all of the meals sales would be attributed to Northampton and none of the meals sales would be attributed to Amherst in the DOR data.

Similarly, sales of meals by restaurants that are part of a national chain may be filed together under the address of the corporate headquarters. If this address is out-of-state, then sales of meals from this chain might not appear in any of the local tallies.

Additional questions about the data may be directed to Office of Tax Policy Analysis, Massachusetts Department of Revenue at 617-626-2100.